Simplify Student Loans

High-level Summary

I validated the concept for a web app with a target user group. After that, I led the research team and contributed to the design of the web app for Dough. Dough is a startup that helps students reduce their student debt while in school, and match graduates with the right payment plans throughout their lives.

Role: Lead UX Researcher and Product Designer

Duration: 1 year, working part-time at the startup Dough

The Challenge

The process of taking out student loans and paying them back is difficult even if students do everything right. Many students automatically accept financial aid packages that aren’t tailored to their needs and they accept the default option. Consequently, students overborrow, on average, $3,000 each year and don’t realize that they can return some, or all of their loans. How can we advise students to make informed borrowing choices?

The Solution

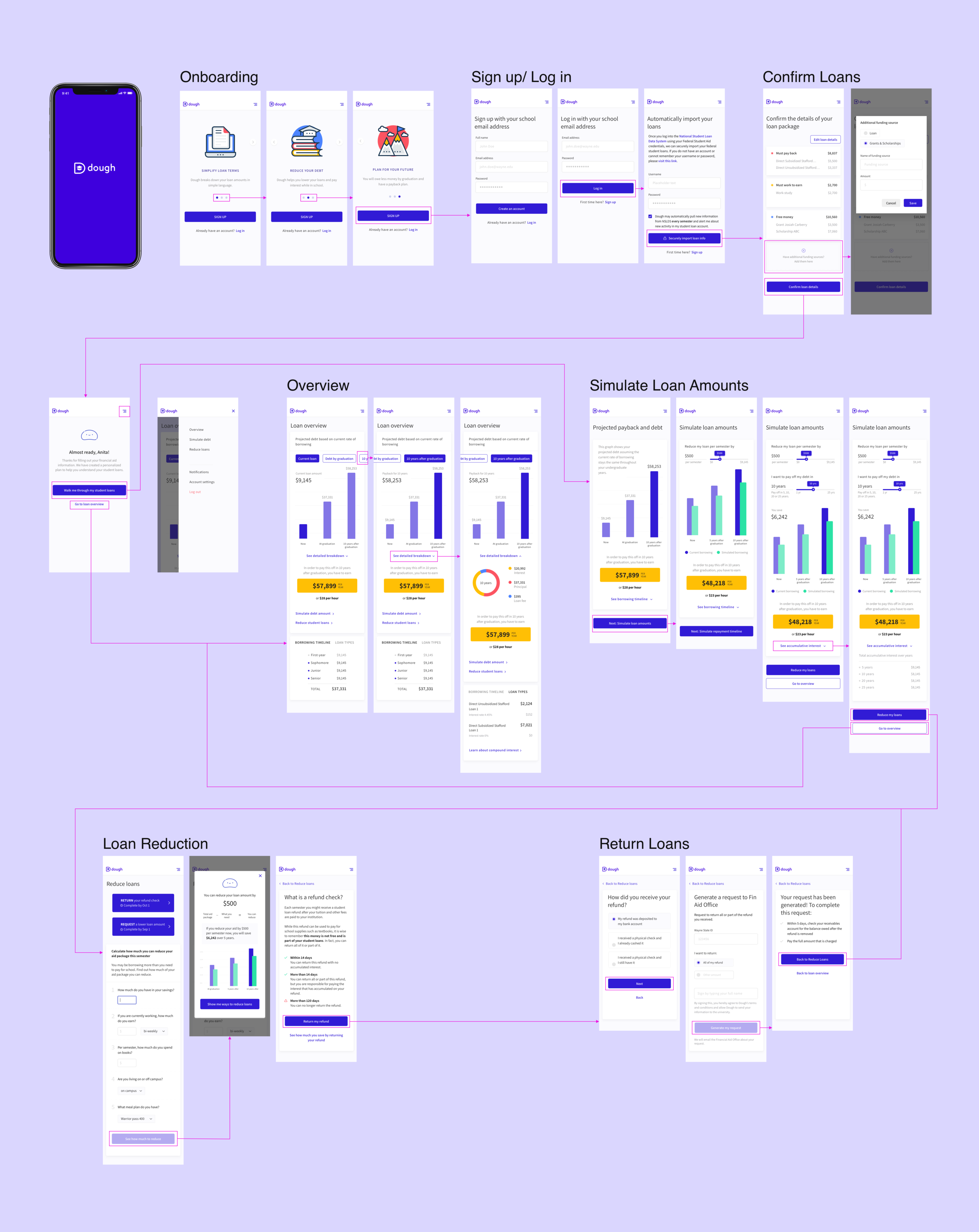

Dough is a web app that equips students to make better financial decisions about how much money to take out in loans each semester.

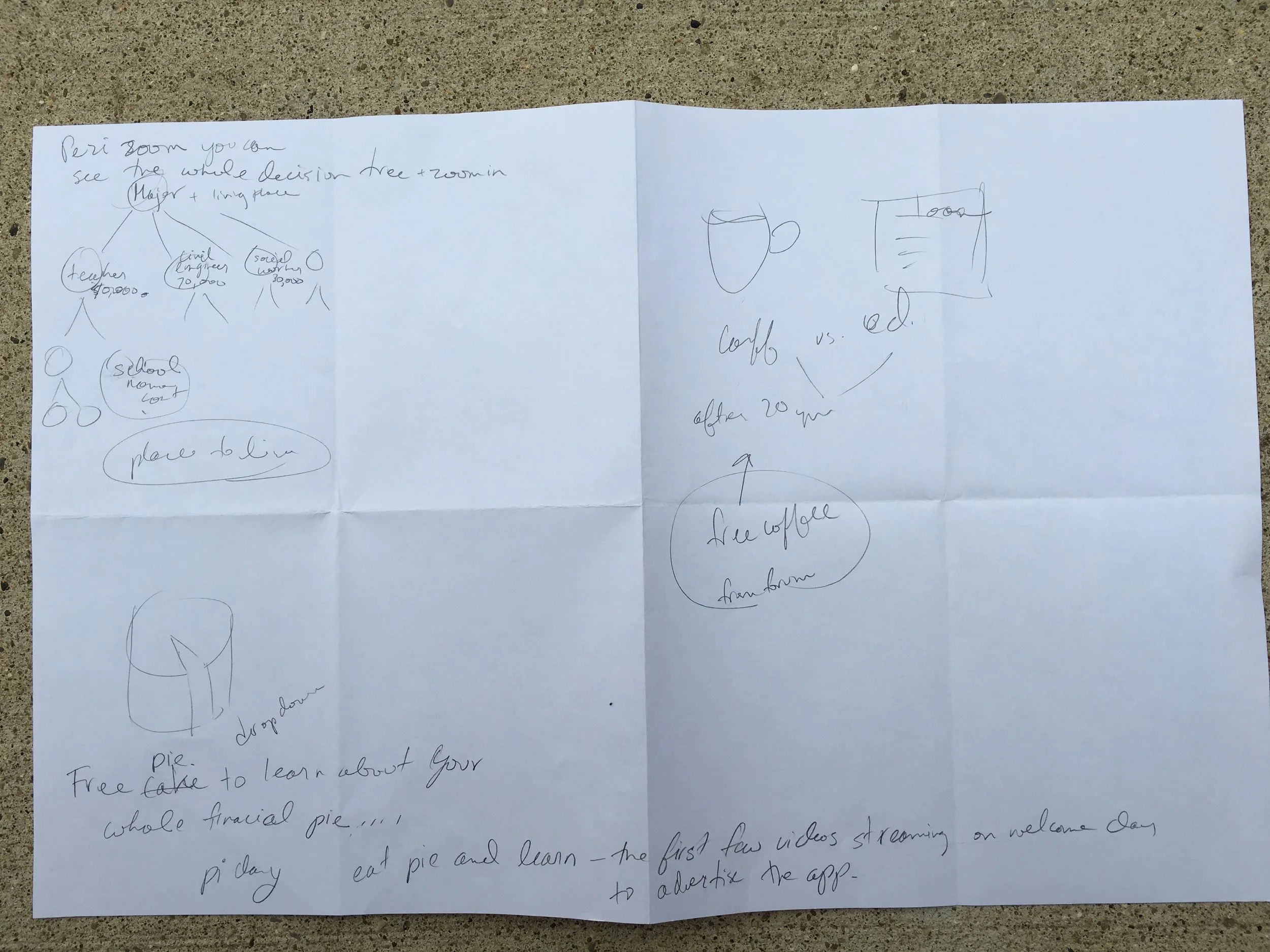

Secondary Research, Ideation & Design Beginnings

The Founder of Dough, Catalina Kaiyoorawongs, had already done secondary research about the student loan crisis in this country. The average student overborrows by $3,000 each year they are in college and universities don’t tailor financial aid packages to students’ needs. As a team, we started brainstorming ideas to help student understand and reduce their student loans.

Generative Research - Are we on the right track?

Research Goals

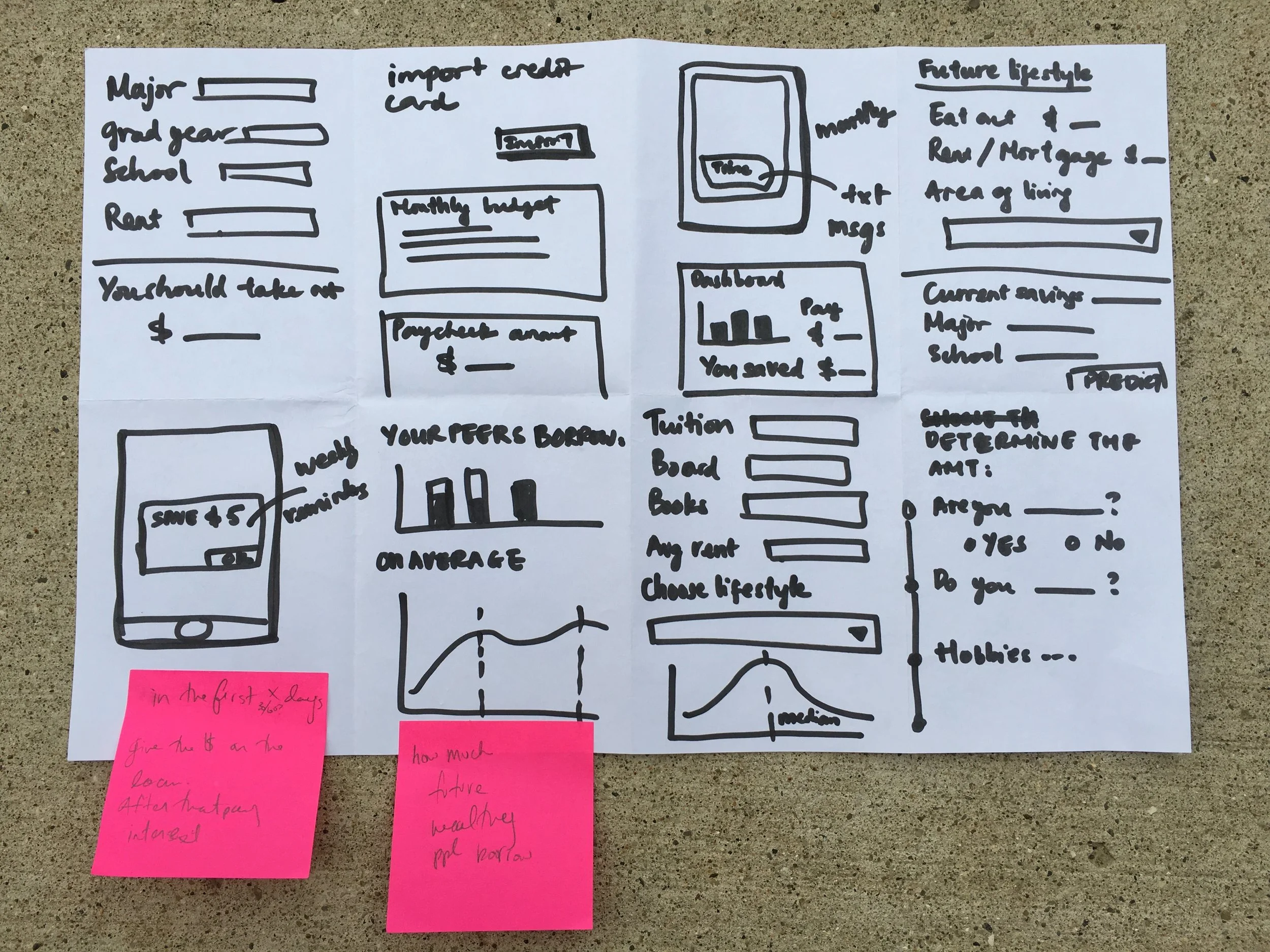

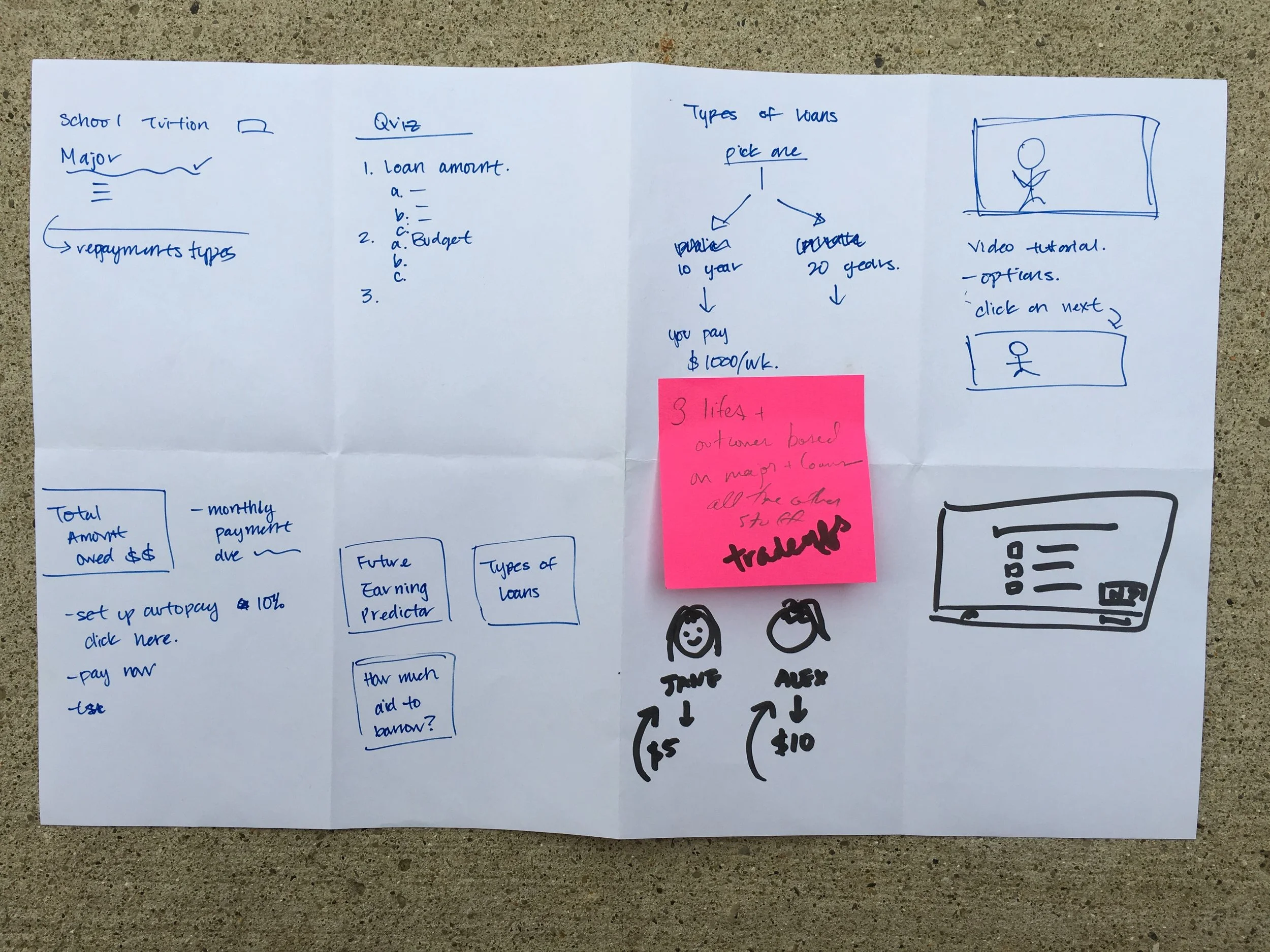

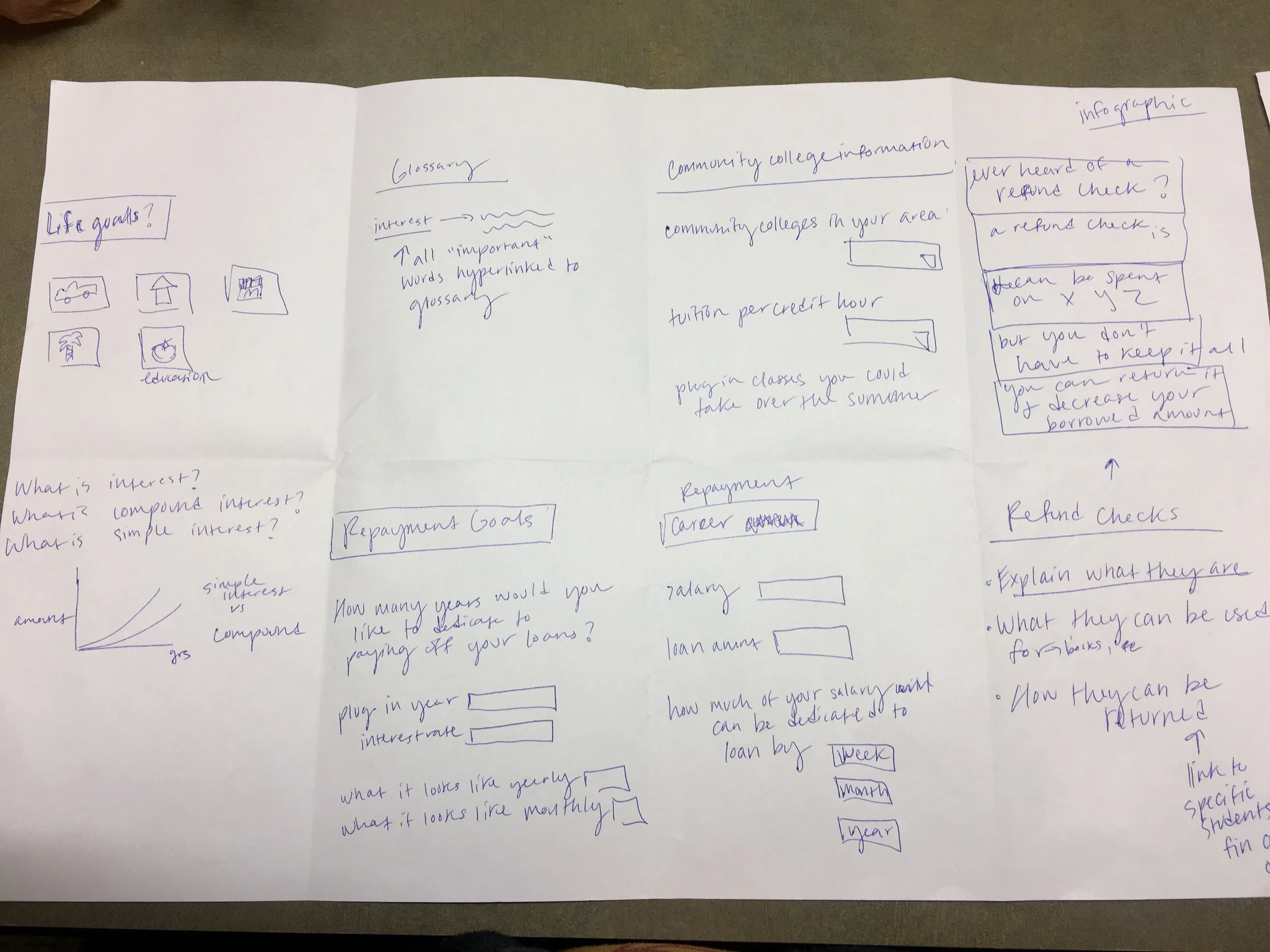

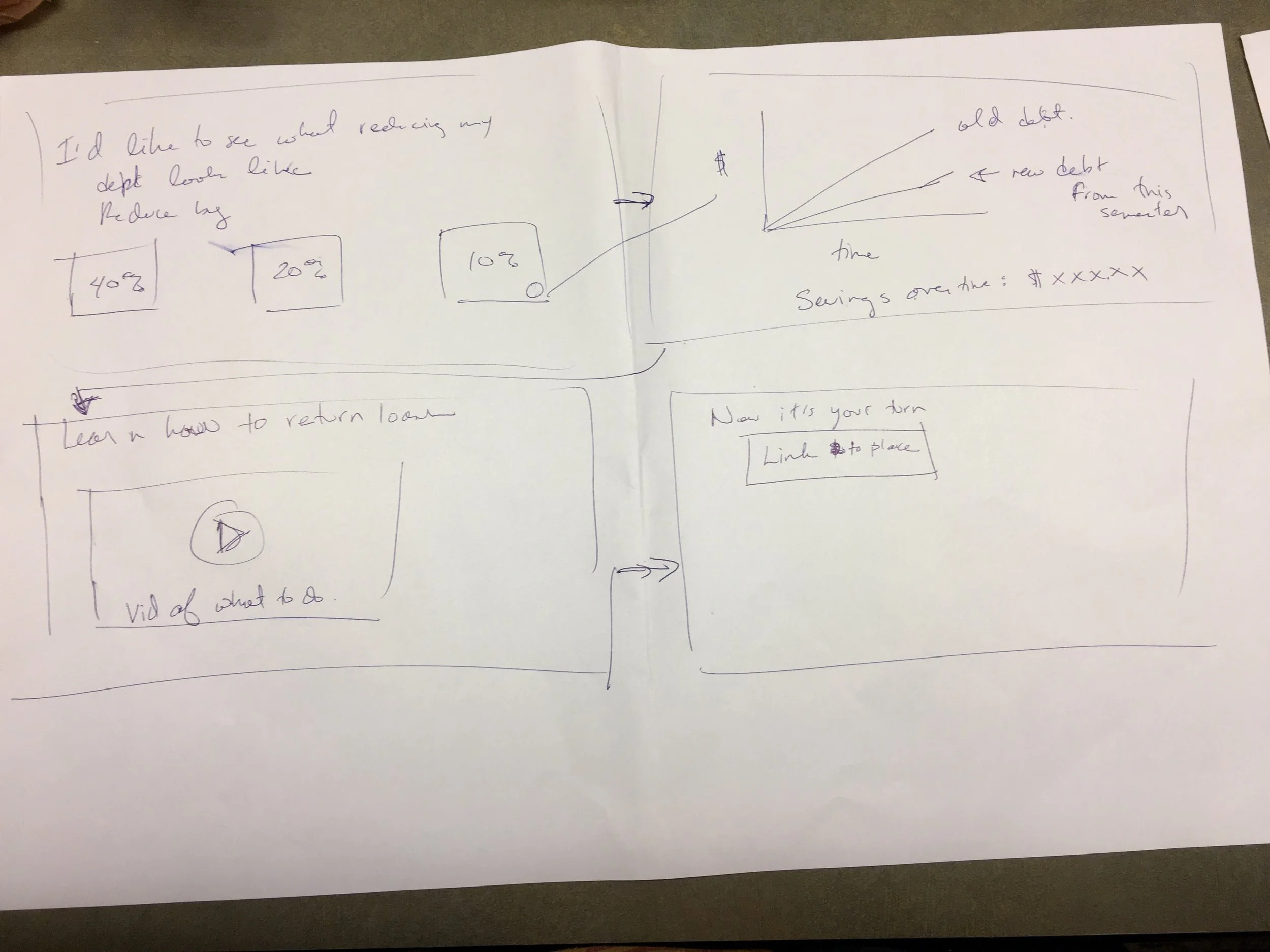

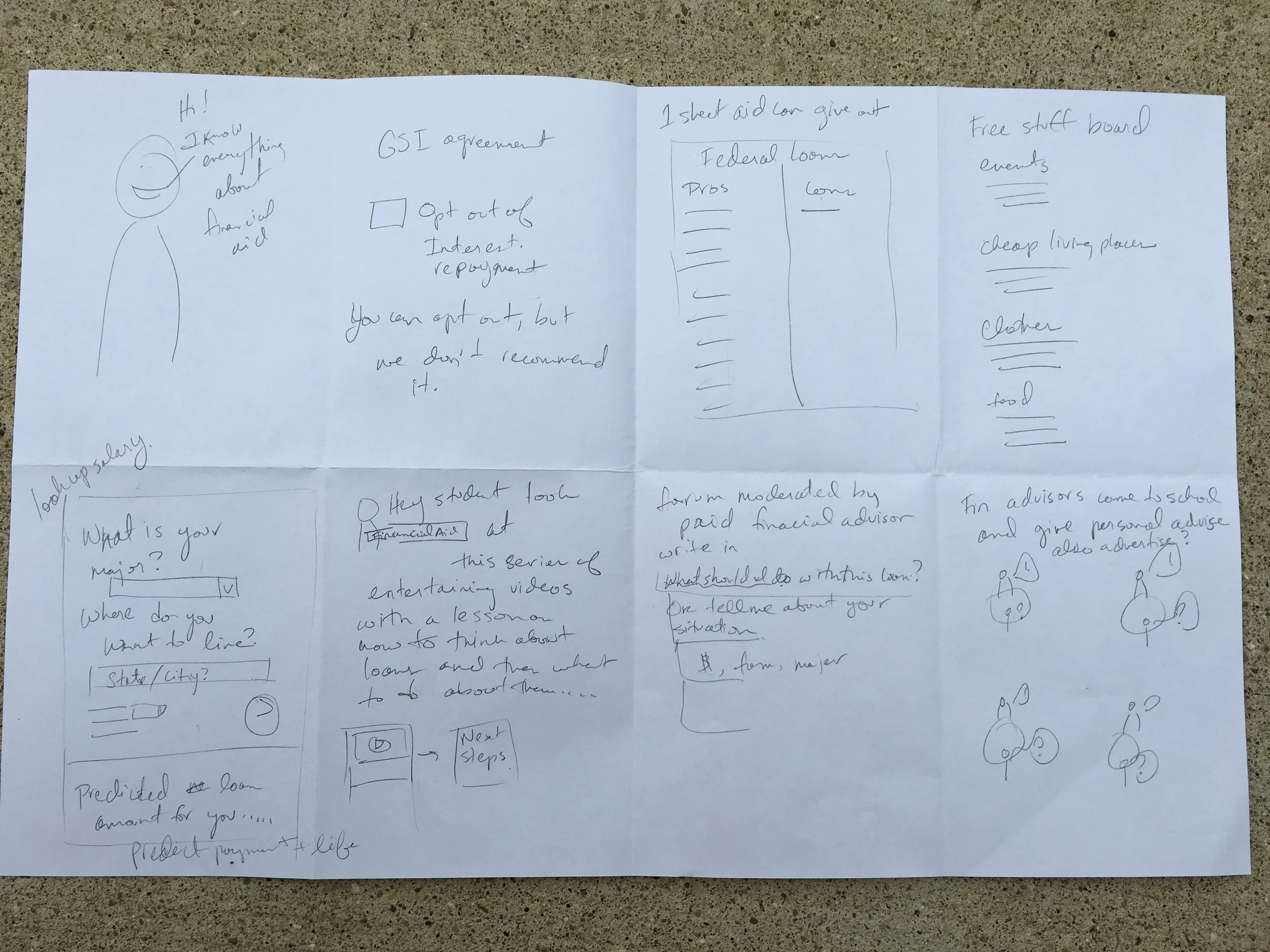

With these initial designs, I developed a research plan to validate the idea of a personal student loan assistant, including a loan reduction calculator and a student debt projection tool. My research goals were the following:

Determine whether students would be interested in using a personal loan assistant to help them manage their student loans.

Learn more about resources and channels students currently use to manage their loans during their undergraduate education.

Get feedback on initial designs.

Methods - Semi-structured Interviews

I chose semi-structured interviews with a little bit of moderated product testing to find the answers our research questions. I chose those methods because it provided immediate, deep insight into undergraduate students’ experience with student loans. I asked about students’ current habits around money and their information seeking behavior around personal finance. Further, I assessed students’ current knowledge of student loans and gathered data about where gaps in their knowledge exist and prevent them from making advantageous decisions about borrowing.

Participants - Wayne State Undergraduate Students with Debt

Our participants were Wayne State undergraduate students with student loan debt. They were our target users for the first phase of our research and design process because Dough had a strategic partnership with Wayne State University for the first release of Dough.

Recruitment Challenges - No Shows

We thought there would be five students lined up to be participants in our user testing at Tech Town in Detroit because of our CEO’s connections there. But 3 out of 5 the people who were supposed show up, didn’t show.

So, we recruited participants in Wayne State’s campus coffee shop by walking up to people and asking if they had student debt and if they had 45 minutes to talk to us in exchange for a $15 Starbucks gift card.

The five participants were university students, sophomores through seniors, with student loan debt, from a variety of majors. We recruited sophomores, juniors and seniors because they already have some experience with student loans.

Findings - Yes, we’re on the right track!

Finding 1: Students’ displayed an overwhelming demand for a personal student loan assistant product. All our participants were interested in staying in touch so that they could use our product when it goes into production.

“Please take down my email address, because I want to use this when it comes out.”

“When do you plan on launching the app? Will I be able to use it? Even if it’s after I graduate?”

“I feel like, a lot of universities, like, don’t tell you a whole lot. And with your parents, if you’re not, like, sitting there talking to them about it, all the way through, you still miss out on a lot of stuff. So I think this would help to fill in the gaps that you don’t get from a university or your parents”

Finding 2: Students can defeat hyperbolic discounting and loss aversion when faced with a greater future loss. Students expressed discomfort about returning any portion of their loans. But after they saw how much money they would lose by not returning a portion of their loan they became much more interested in how much they could return, how that amount was calculated and instructions on how to return it.

Finding 3: All five participants’ main source of information about their loans was their parents and other relatives with debt. Three of five participants also used their loan servicer’s website to learn about their loans. Students had varying knowledge about their student loans based the counseling they had received from their parents and relatives. Some students didn’t know that they could return a part of their loans that semester some students did. None of the students knew that there was a loan fee associated with each loan that was calculated based on the size of the loan.

“I talk to my dad about my loans.”

“My parents and my uncle help me to understand my loans. My uncle still has loans so he knows what he’s talking about.”

Finding 4: Students think bar graphs are clearer than line graphs for showing how a loan grows over time. Students were confused by the line graph. They thought the bar graph was more concise because it showed them how much their total debt would change at important snapshots in time: now, at graduation and in 10 years. People

[About the line graph] “What does this mean?”

[About the bar graph] “This one is clearer, I can see what will happen over time.”

Finding 5: All participants wanted a personalized number telling them how much they could reduce their student loans that semester. This validated our idea for a calculator where students put in their financial aid package information (loans, grants, work study, etc.), and their expenses and receive a recommendation for an amount of money to return. We tried several designs that showed students how much they could reduce their loans. The one that students responded to most positively was a simple subtraction problem:

total aid package - what you need = what you can return

Finding 6: The ROI of students’ education has no bearing on their decisions to take out loans.

“Freshman and sophomores want flexibility with their major. So the loans [they take out] aren’t part of that decision.”

“I’ll take the money out and figure out how to pay it back later”

Personas

I created personas based on the interviews with Wayne State undergraduate students. The aim of the personas was to determine the goals and characteristics of our core user base. We were able to determine that our core group of users were solidly middle class, and they came from a mix of blue collar and white collar families who had a small financial safety net.

Based on the interviews, we determined that students from low income families weren’t our target market. Advising those students came with too high a risk, as a hundred dollars could mean the difference between a student staying in school and dropping out of school that semester. We didn’t want our advising tool to be the reason that students dropped out of school.